Investing in Good Quality Reduces the Cost of Poor Quality

Many companies use a simple pricing equation:

Manufacturing costs + profit margin = price

At first glance, this seems straightforward. In reality, it often hides a major issue. Many companies do not fully understand how much quality-related costs accumulate throughout the production process.

Quality costs are often invisible. They build up slowly across different stages of manufacturing. Without proper analysis, they remain unmanaged.

Jarno Hartikainen, Sparklike’s Development & Quality Manager, has extensive experience in process development and quality improvement. Based on this background, he explains how manufacturers can reduce quality-related costs without compromising product integrity.

Why Quality-Related Costs Deserve More Attention

Managing quality-related costs is difficult when the actual cost factors are not clearly defined. When these costs are carefully identified, measured, and monitored, companies are better positioned to reduce unnecessary expenses, improve gross profit, and strengthen the reliability of their products.

Many organizations focus primarily on reducing costs in general. At the same time, they may overlook the underlying causes of quality-related costs. This often results in short-term savings but limits long-term performance improvements. One effective way to address this challenge is to invest in proper quality control equipment that supports consistent and measurable quality management.

Discover Sparklike’s quality control equipment for gas measurement for insulating glass.

Quality Costs Can Significantly Impact Profitability

It has been estimated that quality-related costs can account for approximately 20% of a company’s annual turnover.

Consider a simplified example:

-

Annual turnover: 100

-

Overall costs: 90

-

Gross profit: 10

To improve profitability, companies usually consider two options: increasing annual turnover or reducing costs. For many manufacturers, doubling turnover is difficult to achieve in practice. Reducing costs is often the more realistic and controllable approach. In this context, quality-related costs are a logical and impactful place to start.

Why Cutting Quality Is the Wrong Way to Cut Costs

Some companies attempt to reduce costs by letting employees go, tightening processes excessively, or aiming only for the minimum acceptable quality level. While this approach may create short-term savings, it often leads to increased customer complaints, additional warranty work, compensations, product returns, and eventually the loss of customer trust. As Jarno Hartikainen points out, these consequences frequently exceed the initial savings gained by lowering production quality.

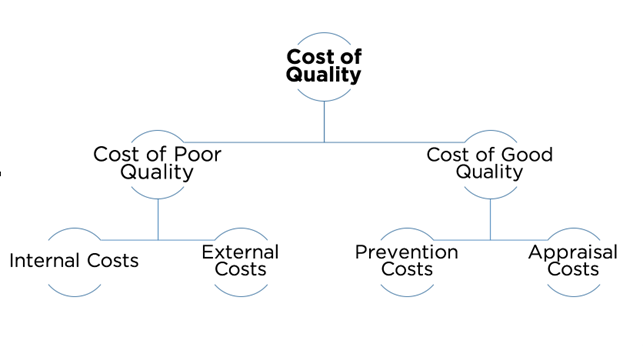

Understanding the Cost of Quality

To better manage quality-related costs, it helps to divide them into two main categories. This model was originally presented by Jack Campanella (1999):

Cost of Poor Quality

-

Internal costs (e.g. scrap, rework)

-

External costs (e.g. returns, claims, warranty work)

Cost of Good Quality

-

Prevention costs

-

Appraisal costs

Campanella shows that investing in prevention and appraisal significantly reduces the cost of poor quality. In practice, one unit of currency invested in prevention or appraisal can reduce poor quality costs many times over.

Practical Ways to Reduce Manufacturing Related Quality Costs

The following areas help companies manage quality-related costs in a structured and effective way. Rather than focusing only on corrective actions, companies should balance preventive measures with systematic evaluation throughout the production process.

To make these cost drivers clearer and easier to manage, they can be divided into seven distinct categories.

Prevention Costs

1. Product or service requirements

Establishment of clear specifications for incoming materials, production processes, finished products, and services.

2. Quality planning

Creation of structured plans for quality, reliability, operations, production, and inspection.

3. Quality assurance

Creation and continuous maintenance of a functioning quality system that supports consistent production quality.

4. Training

Development, preparation, and maintenance of training programs to ensure personnel competence and awareness.

Appraisal Costs

5. Verification

Checking incoming materials, process setups, and finished products against agreed specifications.

6. Quality audits

Confirmation that the quality system is operating as intended and meets defined requirements.

7. Supplier rating

Assessment and approval of suppliers providing products and services critical to production quality.

Investing in Quality Control Pays Off

A clear example of reducing poor quality costs is investing in proper quality control equipment. These investments are often seen as expensive. In reality, the payback period is typically very short.

The saying “Quality is free, but low quality always comes with a price” describes this well.

Example: Quality Control in IGU Manufacturing

Consider a company manufacturing insulating glass units (IGUs).

-

Quality is checked for every 100th unit

-

A known sealing issue affects every 10th unit

As a result:

-

Up to 50% of the insulating gas escapes before shipment

-

The probability of detecting the defect is only 10%

Even if standards allow this level of control, the key question remains: can the company be confident that its products truly meet customer expectations?

Quality Is a Competitive Advantage

Every customer expects reliable quality. A company’s reputation depends on the quality of its products and services.

Saving money by avoiding proper quality control may work in the short term. In the long term, it risks damaging trust, brand value, and competitiveness.

Final Thoughts

In today’s competitive manufacturing environment, accuracy, reproducibility, traceability, and trustworthiness are of critical importance. Customers expect manufacturers to meet prevailing standards and regulations consistently and, above all, to deliver products they can rely on.

As Sparklike’s Development & Quality Manager, Jarno Hartikainen, summarizes: “Customers want to be able to trust in the integrity and ability of the manufacturer to meet prevailing norms and regulations – and most importantly, customer expectations. Time is money, and customers seldom, if ever, can afford to forgive errors.”

By understanding and actively managing quality-related costs, companies can reduce expenses, improve operational performance, and protect their long-term reputation.

Blog updated 6.2.2026